Navigating Economic Ideologies: A Journey Through Time

The concept of the Economy has evolved significantly throughout human history. It literally/ traditionally refers to the system by which goods and services are produced, distributed, and consumed in a society. It also encompasses the mechanisms through which resources are allocated, and the study of how individuals, businesses, and governments make choices to satisfy their needs and wants given scarce resources. The contemporary economies are complex and multifaceted thus the definition of the economy has also evolved in response to technological advancements, changes in political and social structures, and shifts in economic theories.

The traditional understanding often emphasizes the role of markets, production efficiency, and resource allocation as central components of economic systems. While the contemporary understanding of the economy incorporates a wide range of factors, reflecting the interconnectedness of nations, the influence of technology, and the recognition of environmental and social considerations. Let us trace the journey of these ever-changing conceptions over time from the very beginning.

Ancient Times:

Barter System:

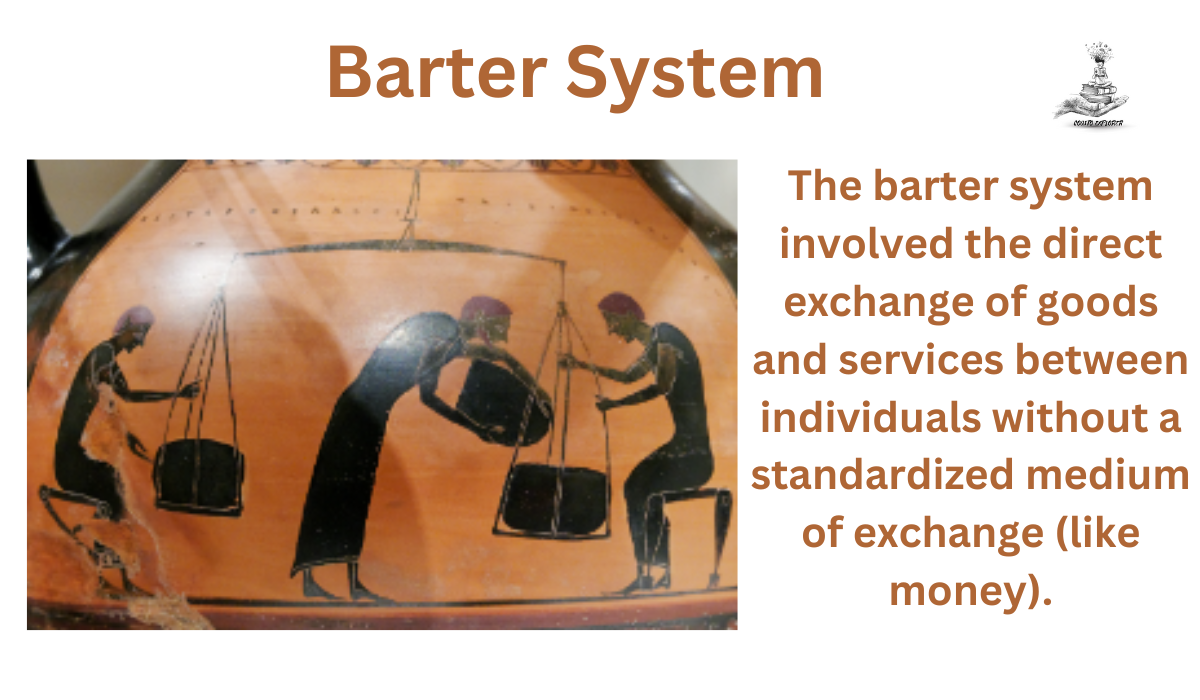

In early civilizations, people engaged in barter trade. The barter system involved the direct exchange of goods and services between individuals without a standardized medium of exchange (like money). While barter was practical for simple transactions, it had limitations such as the double coincidence of wants, lack of standardized value, and difficulties in divisibility, storage, and transportation.

Historically, barter was common in early human societies, along trade routes like the Silk Road, and in colonial America due to the scarcity of currency. However, the limitations of the barter system led to the development of monetary systems, making transactions more efficient and expanding the possibilities for economic exchange.

Agrarian Economies:

Agriculture was the primary economic activity in ancient societies, with communities relying on the cultivation of crops and the domestication of animals. In ancient civilizations, such as the Indus Valley, Mesopotamia, Egypt, and China, agrarian economies formed the basis of society.

In these societies, the majority of the population engages in farming, relying on traditional methods and often practicing subsistence agriculture. Agrarian economies are associated with a rural lifestyle, seasonal farming cycles, and a limited focus on market exchange. The surplus food production also allowed for the development of non-agricultural activities. It has several advantages including food security and potentially sustainable practices but there are several challenges that it faces including limited productivity and vulnerability to environmental changes.

Formal Economy: Concept and Foundation

Ancient economic thinkers from various civilizations, including Aristotle, Plato, Xenophon, Chanakya, Zhuangzi, etc. shaped early economic thought with their philosophical reflections. Aristotle distinguished between natural and unnatural wealth, emphasizing just distribution. Plato critiqued excessive materialism and explored justice in the organization of an ideal state. Xenophon discussed household management and virtues in economic matters. Chanakya, in Arthashastra, addressed statecraft, governance, and economic policies in ancient India.

Zhuangzi, a Daoist philosopher, emphasized spiritual fulfillment over material wealth. These thinkers laid the foundation for early economic principles, considering the ethical, just, and spiritual dimensions of economic activities.

Classical Era:

Mercantilism:

Mercantilism, prevalent from the 16th to 18th centuries, was an economic theory characterized by a focus on accumulating precious metals, particularly through a positive balance of trade. Core principles included protectionism, colonialism, and government intervention to promote domestic industries. Protectionist measures, like tariffs, were implemented to achieve economic goals. The policy framework aimed to maximize a nation’s wealth by favoring exports over imports and establishing colonies. Mercantilism gradually gave way to classical economics in the 18th century, with thinkers like Adam Smith challenging its principles. Despite its flaws, mercantilism had a lasting impact on economic policies and historical developments.

Physiocrats:

The Physiocrats were a group of French economists in the 18th century who laid the foundation for modern economic thought. Led by François Quesnay, they emphasized the importance of natural economic laws and advocated for a laissez-faire approach, arguing that minimal government interference would allow markets to regulate themselves. The Physiocrats identified agriculture as the only productive sector, creating a concept of net product as the source of wealth. They influenced economic policy in France during the reign of Louis XV. Despite criticism for their narrow focus on agriculture, the Physiocrats significantly contributed to the evolution of economic theory, paving the way for later schools of thought such as classical economics.

Industrial Revolution:

Laissez-faire Capitalism:

With the Industrial Revolution, there was a shift from agrarian economies toward industrial and the time witnessed the rise of capitalism. Adam Smith, a key figure in classical economics, argued for Laissez-faire capitalism which is an economic system characterized by minimal government intervention in the marketplace. His book “The Wealth of Nations” (1776) laid the foundation for classical economic thought. Rooted in classical liberalism, it emphasizes limited government involvement, individual freedom, protection of property rights, and reliance on free market mechanisms. The system promotes competition, the profit motive, and consumer sovereignty, with the belief that these elements contribute to economic prosperity and efficiency.

Laissez-faire capitalism has faced criticism for potential income inequality, market failures, and social and environmental concerns. In the modern context, many economies are mixed, incorporating both laissez-faire principles and government intervention. The ideology continues to influence economic debates, with advocates emphasizing the benefits of free markets and critics calling for measures to address potential drawbacks.

Marxian Socialism:

Marxian socialism, developed by Karl Marx and Friedrich Engels, is a socio-economic and political theory that envisions a transition to communism. They critiqued capitalism in works like The Communist Manifesto (1848) and Das Kapital. Their ideas laid the foundation for socialist and communist economic theories.

Marxian socialism is rooted in a materialist conception of history, historical dialectical materialism, and the notion of class struggle between the bourgeoisie (owners of the means of production) and the proletariat (working class). Marx’s analysis of the capitalist mode of production highlights exploitation, alienation, and wealth concentration. The theory predicts a historical progression from capitalism to socialism, involving the dictatorship of the proletariat as a transitional phase towards communism. They envisioned a proletarian revolution leading to a classless society. They face criticisms due to concerns about authoritarianism and the economic calculation problem. Marxian socialism has influenced social movements, academic discourse, and various evolutions, including democratic socialism and post-Marxist theories.

20th Century:

Keynesian Economics (20th century):

Keynesian economics, developed by John Maynard Keynes, is a 20th-century economic theory that emerged in response to the Great Depression. It emphasizes the importance of aggregate demand, effective demand, and the multiplier effect in determining economic outcomes. Keynesian economics advocates for an active role of government in managing the economy through fiscal policy, particularly during economic downturns or to prevent them.

The theory highlights the role of consumption, saving, and liquidity preference in shaping economic activity. Keynesian policies are counter-cyclical, aiming to stabilize the economy by adjusting government spending and taxes. Keynesian ideas have had a lasting impact on economic policy, and the theory continues to influence discussions on macroeconomic management and stabilization.

Mixed Economies:

A mixed economy combines elements of both market and planned economies, seeking a balance between the efficiency of market forces and government intervention to address social inequalities and market failures. Basically, it combines the elements of capitalism and socialism, with varying degrees of government involvement in economic activities.

The private enterprises operate alongside publicly owned or regulated essential services. Governments actively intervene to stabilize the economy, implement social welfare programs, regulate industries, and provide infrastructure. Progressive taxation and a focus on social welfare are common features. The mixed economy model gained prominence post-World War II, with flexibility, economic efficiency, and social welfare as advantages. Critics raise concerns about bureaucracy, market distortions, and political challenges. The specific mix varies among countries, reflecting diverse social, cultural, and historical contexts.

Contemporary Times:

Globalization:

Globalization is the increasing interconnectedness and integration of economies, societies, and cultures on a global scale. It involves the flow of goods, services, information, technology, capital, and people across national borders. Core aspects include international trade, foreign direct investment, technological advancements, cultural exchange, and global supply chains. Drivers include technological advancements, liberalization of trade and investment, and the activities of multinational corporations. However, globalization has faced criticisms for contributing to inequality, cultural homogenization, environmental impact, and job displacement. Responses include regionalism, calls for global governance, and a resurgence of interest in localism. Globalization has profound implications for economies, societies, and cultures worldwide, presenting both opportunities and challenges.

Technology and Information Age:

The Technology and Information Age, often referred to as the Digital Age. It is characterized by the rapid advancement and widespread adoption of information and communication technologies (ICTs). This era has seen the emergence of the internet, mobile devices, social media, and various digital innovations that have profoundly impacted diverse aspects of human life. The core aspects include increased connectivity, digitalization, and the prevalence of online platforms in areas such as business, education, healthcare, and entertainment.

Historical milestones include the development of personal computers, the expansion of the internet, and the mobile revolution. The Information Age has brought about transformative changes in communication, business models, education, healthcare, and entertainment. It has also presented challenges, including the digital divide, cybersecurity threats, and concerns about job displacement. The ongoing evolution of the Technology and Information Age continues to shape human progress and societal dynamics.

Environmental and Social Considerations:

Environmental and social considerations are critical factors in shaping responsible and sustainable practices across various domains. On the environmental front, efforts focus on addressing climate change, conserving biodiversity, sustainable resource management, waste reduction, and transitioning to clean energy. Social considerations emphasize social equity, labor rights, fair wages, community engagement, human rights, ethical business practices, health and safety, and cultural sensitivity. The interconnectedness of environmental and social aspects is evident in initiatives like Corporate Social Responsibility (CSR), impact assessments, and the integration of sustainability into global supply chains. Challenges include balancing economic development with environmental conservation and social equity. Global cooperation, technological innovation, and education are identified as opportunities to address these challenges and build a sustainable and inclusive future. Awareness and commitment to these considerations are essential for fostering responsible practices and achieving positive outcomes for both people and the planet.

Financialization:

Financialization is a transformative trend characterized by the increasing influence of financial markets (money and capital markets) and motives in the global economy. It involves the rise of financial institutions, a focus on short-term profits, financial engineering, securitization, and continuous financial innovation. The historical factors such as deregulation and globalization have facilitated this process. Financialization has significant impacts, including income inequality, a shift in corporate behavior towards short-term gains, financial instability, and a potential diversion of resources from the real economy. The concept faces criticism for short-termism, lack of accountability, and excessive risk-taking. There have been calls for regulation of financial markets and institutions to ensure stability and protect against systemic risks, the promotion of sustainable finance, and corporate governance reforms to align financial activities with broader societal goals. The phenomenon raises ongoing discussions about the balance between financial activities and sustainable, inclusive economic development.

Conclusion:

The evolution of economic systems and thought from ancient times to the contemporary era reflects a dynamic interplay of various factors, philosophies, and ideologies. The traditional barter system paved the way for the development of monetary economies, leading to more complex systems and the rise of capitalism, socialism, and mixed economies. Throughout history, economic thinkers (Aristotle, Chanakya, Adam Smith, Karl Marx, John Maynard Keynes) and theories have influenced economic structures and policies. In the modern era, globalization has emerged as a defining force, fostering interconnectedness and influencing economic, social, and cultural aspects on a global scale. The Technology and Information Age further accelerated this interconnectedness, revolutionizing communication, business, education, and healthcare.

The discussion on financialization highlights the contemporary trend of increased financial influence, impacting corporate behavior, income distribution, and the overall stability of economies. As we navigate the complexities of the modern economic landscape, finding a balance between economic growth, social equity, and environmental sustainability is paramount. Calls for responsible financial practices, ethical considerations, and global cooperation underscore the need for a holistic approach to address the challenges and opportunities presented by the evolving economic systems and ideologies. It is within this context that ongoing dialogues, regulatory frameworks, and innovative solutions will shape the trajectory of future economic development.